Legal Updates

November 23, 2020

Proposition 19: Important Change to Rules Regarding Transfers of Real Property

Proposition 19: Important Change to Rules Regarding Transfers of Real Property

As many of you may be aware, California Proposition 19 (“Prop 19”), which passed on November 3, 2020, completely eliminates the parent-child exclusion from reassessment for all properties other than a parent’s principal residence, which is used by the child as a principal residence within one (1) year of the date of transfer (in some limited cases grandparent-grandchild transfers also benefit from this exclusion).

Prior to the effective date of Prop 19 on February 16, 2021, a parent can transfer their principal residence and up to $1,000,000 of assessed value of other property (including commercial properties, rental properties, vacation homes, etc.) to their child, free from reassessment.

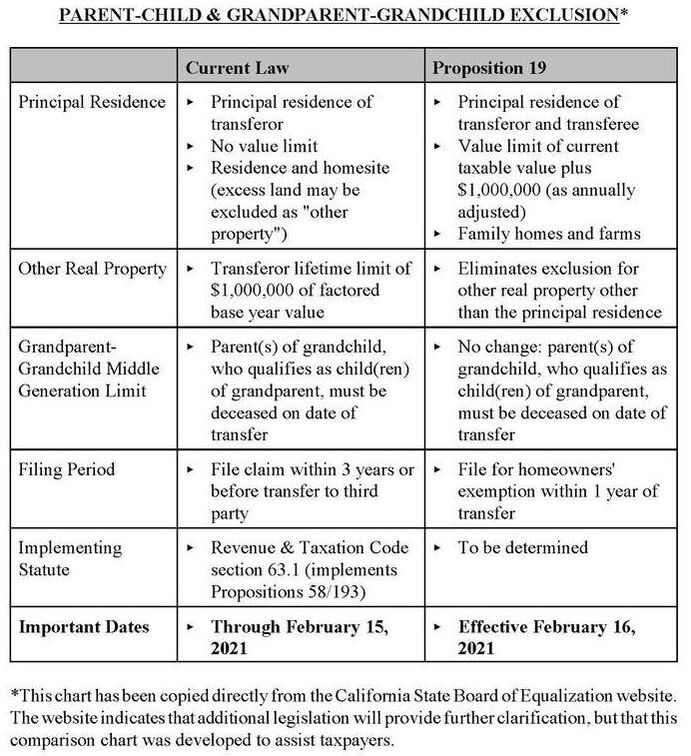

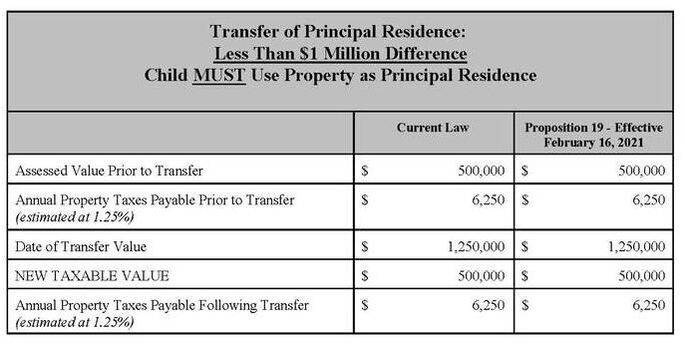

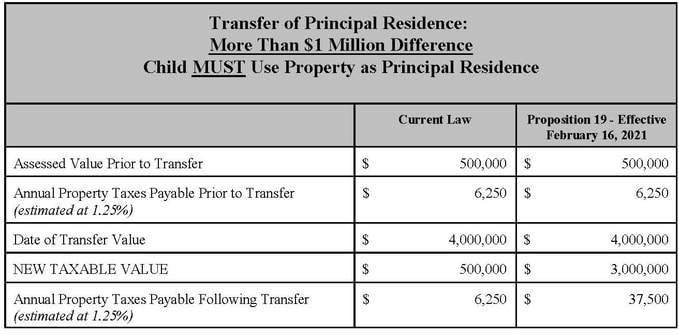

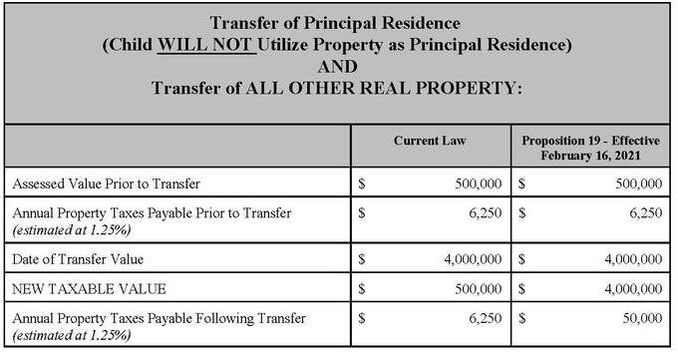

As detailed in the first chart below, developed by the California Board of Equalization, beginning on February 16, 2021, Prop 19 will eliminate parent-child exclusions from reassessment except in cases where a principal residence of a parent is transferred to the child (or in some cases to a grandchild) and the property will be used as the child’s principal residence. Furthermore, any such exclusion of reassessment will now be limited to $1 million. In the additional charts provided below we have illustrated the possible property tax consequences of these new rules.

This will be a marked change to the parent-child exclusion that will result in major increases in the annual property taxes of transferred or inherited real property.

Due to these unprecedented times, the Assessor’s Office and the Recorder’s Office have been experiencing delays for even routine matters. Therefore, please contact our office as soon as possible if you would like to learn more about this change in the law, or if you would like to discuss the possibility of transferring real property to your child(ren) prior to the effective date of Prop 19, February 16, 2021, in order to take advantage of the current unlimited exclusion for your principal residence, and/or your $1,000,000 exclusion available for other properties.

Prior to the effective date of Prop 19 on February 16, 2021, a parent can transfer their principal residence and up to $1,000,000 of assessed value of other property (including commercial properties, rental properties, vacation homes, etc.) to their child, free from reassessment.

As detailed in the first chart below, developed by the California Board of Equalization, beginning on February 16, 2021, Prop 19 will eliminate parent-child exclusions from reassessment except in cases where a principal residence of a parent is transferred to the child (or in some cases to a grandchild) and the property will be used as the child’s principal residence. Furthermore, any such exclusion of reassessment will now be limited to $1 million. In the additional charts provided below we have illustrated the possible property tax consequences of these new rules.

This will be a marked change to the parent-child exclusion that will result in major increases in the annual property taxes of transferred or inherited real property.

Due to these unprecedented times, the Assessor’s Office and the Recorder’s Office have been experiencing delays for even routine matters. Therefore, please contact our office as soon as possible if you would like to learn more about this change in the law, or if you would like to discuss the possibility of transferring real property to your child(ren) prior to the effective date of Prop 19, February 16, 2021, in order to take advantage of the current unlimited exclusion for your principal residence, and/or your $1,000,000 exclusion available for other properties.

We have drafted the following charts depicting various scenarios to help illustrate the property tax consequences of a parent-child (or limited grandparent-grandchild) transfer of real property under both current law and under Prop 19, which will take effect on February 16, 2021.

March 2020

Estate Planning and SECURE Act Considerations in 2020

Estate Planning and SECURE Act Considerations in 2020

We would like to make you aware of a major change to the laws governing defined contribution plans and IRAs as well as address recent legislative proposals and the sunset of the 2017 Jobs Act. One or all of these developments is likely to affect your estate plans in the coming years.

As will be detailed below, it is imperative that all clients (1) review their beneficiary designation forms for any retirement plans or IRAs, (2) review and revise Conduit Trusts currently in existence, (3) reevaluate the income tax repercussions of selecting particular beneficiaries, and (4) review trusts for surviving spouses that are the named beneficiaries of any retirement plans or IRAs.

Estate and Tax Law Developments:

As you most likely are aware, the 2017 Jobs Act doubled the estate and gift tax exemption from $5,000,000 to $10,000,000, with a cost of living increase. The estate and gift tax exemption today is $11,580,000 per person ($23,160,000 per couple), but this doubled exemption will sunset at the end of 2025, and this estate and gift tax exemption will be cut in half. If a client is in a position to make large lifetime gifts, it may be advisable to do so before the sunset in order to get the maximum benefit out of the increased exemption before it expires. The IRS has indicated that this is an option and that assets given away under the increased exemption will not be pulled back into estates to be taxed.

While the 2017 Tax Cut and Jobs Act gave the business community, real estate investors and most high income taxpayers major tax reductions, charities did not benefit. With the increased standard income tax deduction, most people are no longer itemizing deductions, and people who do not give to charity receive the same deduction as those who do contribute.

Clients now need to plan carefully for gifts to charity. The common wisdom is to plan charitable gifts for years in which you itemize your deductions (i.e. a year with significant medical expenses or large charitable gifts) so that the charitable gift will be tax deductible. Another strategy may be to make a charitable gift to a Donor Advised Fund. Distributions from the fund can then be parceled out over years in which you take the standard deduction.

Additionally, in 2015, Congress passed the IRA Charitable Rollover Act, allowing you to rollover up to $100,000 a year from your IRA to charity tax-free as a “Qualified Charitable Distribution,” or QCD. Even post SECURE Act, this tax benefit is a valuable way to make gifts to charity.

SECURE Act:

The SECURE Act has been in effect since January 1, 2020. The SECURE Act governs defined contribution plans and IRAs. Firstly, it changes the required beginning date for distributions from such plans from age 70½ to age 72. However, the most dramatic result of the SECURE Act is the new ten-year minimum required distribution regime, which only has a few important exceptions for Eligible Designated Beneficiaries (“EDBs”). If distributions are not taken from a defined contribution plan or IRA account before the end of the 10th year, the remaining funds in any such account will be subject to a 50% penalty.

This new rule effectively eliminates stretch planning (i.e. distributions taken over the life expectancy of the beneficiary) for retirement benefits. Only Participants in retirement plans, owners of IRAs, their spouses, and other EDBs can continue to use the unified table to defer distributions over their life expectancies. All other death beneficiaries will now be subject to a ten-year distribution rule (i.e. they must take out the entire account over a period of ten years). As a result, it is now urgent to review all beneficiary forms to address the ten-year rule. For persons who died before 2020, the old rules apply, except that even for pre-SECURE Act deaths, the new ten-year distribution rules will take effect upon the designated beneficiary’s subsequent death.

“See Through Trusts” are trusts for individuals which can be treated in the same way as individual beneficiaries. A See Through Trust can be a trust for a single individual called a conduit trust or it can be an accumulation trust for more than one individual beneficiary. The Act still recognizes See Through Trusts, but except for certain trusts for EDBs, these See Through Trusts will now also be subject to the ten-year distribution rule for all persons dying after December 31, 2019.

There are five categories of EDBs:

SECURE Act Recommendations:

As a result of the SECURE Act, IRA and retirement plan beneficiary forms will have major tax consequences. Our main recommendations are as follows:

As always, tax and trust law is subject to change. Proposals of a reduction of the federal estate tax exemption to $3,500,000, higher progressive rates on estates, elimination of stepped-up basis upon death, and even the possible imposition of a California estate tax have all been considered by lawmakers.

We are dedicated to the planning and administration of estates for generations to come. We strive to understand and implement the goals of our clients as much as possible. It is our continued pleasure to spend time with our clients to adapt their wishes to the changing tax laws.

If you have an IRA or retirement plan we recommend more than anything else that you obtain from the IRA custodian or plan administrator a copy of the current beneficiary form. We urge all clients to send us copies of these forms.

As will be detailed below, it is imperative that all clients (1) review their beneficiary designation forms for any retirement plans or IRAs, (2) review and revise Conduit Trusts currently in existence, (3) reevaluate the income tax repercussions of selecting particular beneficiaries, and (4) review trusts for surviving spouses that are the named beneficiaries of any retirement plans or IRAs.

Estate and Tax Law Developments:

As you most likely are aware, the 2017 Jobs Act doubled the estate and gift tax exemption from $5,000,000 to $10,000,000, with a cost of living increase. The estate and gift tax exemption today is $11,580,000 per person ($23,160,000 per couple), but this doubled exemption will sunset at the end of 2025, and this estate and gift tax exemption will be cut in half. If a client is in a position to make large lifetime gifts, it may be advisable to do so before the sunset in order to get the maximum benefit out of the increased exemption before it expires. The IRS has indicated that this is an option and that assets given away under the increased exemption will not be pulled back into estates to be taxed.

While the 2017 Tax Cut and Jobs Act gave the business community, real estate investors and most high income taxpayers major tax reductions, charities did not benefit. With the increased standard income tax deduction, most people are no longer itemizing deductions, and people who do not give to charity receive the same deduction as those who do contribute.

Clients now need to plan carefully for gifts to charity. The common wisdom is to plan charitable gifts for years in which you itemize your deductions (i.e. a year with significant medical expenses or large charitable gifts) so that the charitable gift will be tax deductible. Another strategy may be to make a charitable gift to a Donor Advised Fund. Distributions from the fund can then be parceled out over years in which you take the standard deduction.

Additionally, in 2015, Congress passed the IRA Charitable Rollover Act, allowing you to rollover up to $100,000 a year from your IRA to charity tax-free as a “Qualified Charitable Distribution,” or QCD. Even post SECURE Act, this tax benefit is a valuable way to make gifts to charity.

SECURE Act:

The SECURE Act has been in effect since January 1, 2020. The SECURE Act governs defined contribution plans and IRAs. Firstly, it changes the required beginning date for distributions from such plans from age 70½ to age 72. However, the most dramatic result of the SECURE Act is the new ten-year minimum required distribution regime, which only has a few important exceptions for Eligible Designated Beneficiaries (“EDBs”). If distributions are not taken from a defined contribution plan or IRA account before the end of the 10th year, the remaining funds in any such account will be subject to a 50% penalty.

This new rule effectively eliminates stretch planning (i.e. distributions taken over the life expectancy of the beneficiary) for retirement benefits. Only Participants in retirement plans, owners of IRAs, their spouses, and other EDBs can continue to use the unified table to defer distributions over their life expectancies. All other death beneficiaries will now be subject to a ten-year distribution rule (i.e. they must take out the entire account over a period of ten years). As a result, it is now urgent to review all beneficiary forms to address the ten-year rule. For persons who died before 2020, the old rules apply, except that even for pre-SECURE Act deaths, the new ten-year distribution rules will take effect upon the designated beneficiary’s subsequent death.

“See Through Trusts” are trusts for individuals which can be treated in the same way as individual beneficiaries. A See Through Trust can be a trust for a single individual called a conduit trust or it can be an accumulation trust for more than one individual beneficiary. The Act still recognizes See Through Trusts, but except for certain trusts for EDBs, these See Through Trusts will now also be subject to the ten-year distribution rule for all persons dying after December 31, 2019.

There are five categories of EDBs:

- Spouse. A spouse is an EDB and will always have a number of options. A spouse can still rollover a retirement benefit or elect to treat it as his or her own. Different kinds of trusts for a spouse can produce dramatically different results. A conduit trust can allow the spouse to defer distributions over the life expectancy of the spouse in accordance with the single life table. A non-conduit trust for a spouse may require the use of a fixed-term (or reduce-by-one) method of distribution which may cause the entire IRA to be distributed years before the spouse dies. If you have retirement benefits payable to a trust for a surviving spouse, this trust should now be reviewed. Under the SECURE Act, when a surviving spouse dies, the ten-year rule will be applicable to subsequent beneficiaries.

- Minor Child. Benefits for a minor child can be paid out over the single life table until the child reaches the age of majority (variously defined as 18, 21 and 26). A child can be treated as a minor if the child has not completed a specified course of education and is under the age of 26. After attainment of the age of majority by the minor child, the ten-year rule becomes applicable unless the child qualifies as disabled or chronically ill. Again, any trust designed to hold retirement benefits for a minor child should be reviewed to ensure that the ten-year distribution rule can be delayed until majority. Some trusts as currently drafted may require that the ten-year rule start immediately upon the IRA owner’s death.

- Disabled Person. This is a person who is unable to engage in any substantial gainful activity by reason of a medically determinable physical or mental impairment which can be expected to result in death or be of long-continued and indefinite duration. It is important to know that a properly drafted trust or subtrust for a disabled person can be a way to stretch out distributions over the life expectancy of a disabled person. After the disabled person dies, the distribution can pass to others over ten years.

- Chronically Ill Individual. A person who is certified to have an illness of indefinite duration which is reasonably expected to be lengthy in nature qualifies as a chronically ill individual. A properly drafted trust or subtrust for a chronically ill person can also qualify for the stretch out and avoid the ten-year distribution rule.

- Less Than 10 Years Younger. Any person who is less than ten years younger than the IRA owner can be an EDB. This may work well for siblings, other relatives, and friends of relatively the same age as an IRA owner or retirement plan participant. Since a See Through Trust would be treated as the individual beneficiary, such a trust for a less than 10 year younger beneficiary would also avoid the ten-year distribution rule.

SECURE Act Recommendations:

As a result of the SECURE Act, IRA and retirement plan beneficiary forms will have major tax consequences. Our main recommendations are as follows:

- Review all beneficiary forms carefully. Please request current beneficiary forms from your retirement plan providers. We strongly recommend reviewing these forms with us to make sure that your wishes are being accomplished and that you are in a good position under the new rules. This may involve creating customized beneficiary forms to provide to the custodians of your plans.

- Conduit Trusts. A conduit trust is a trust which requires all IRA distributions to the trust to be paid out to the beneficiary. The major benefit of a conduit trust was always the stretch-out, because distributions to a conduit trust could be made over the life expectancy of the sole beneficiary. The SECURE Act changes this. Conduit trusts need immediate attention and will need to be reviewed and revised.

- Analysis of Appropriate Beneficiaries: (A) High vs. Low Income Beneficiaries. It may be best to target distributions of regular IRAs to those who are in low income tax brackets and/or to beneficiaries outside of California. High income beneficiaries may be subject to high income taxes unless steps are taken to designate appropriate beneficiaries and to spread out distributions. (B) Review Trusts as Possible Beneficiary. It may be beneficial to name trusts which allow accumulations of income and sprinkling of distributions. (C) Charitable Giving. If you have charitable intent, consider charitable remainder trusts for charities as a beneficiary of your IRA in order to defer taxes over a beneficiary’s life expectancy or period of years. An individual beneficiary could get a set percentage of the trust every year and a charity would be the ultimate beneficiary of such trust.

- Tax Considerations: (A) Roth IRA Option. Also consider converting some of your regular IRAs to Roth IRAs. (B) Life Insurance. You may consider life insurance as a way to pay taxes on your IRA and retirement accounts. (C) Specialized Tax Provisions in Documents. We recommend including special tax provisions in your estate planning documents to allocate the tax liabilities where it makes tax sense.

- Disclaimer Option. Until now it has been a common practice to name a child as the primary beneficiary of an IRA and to name conduit trusts for the child’s issue or grandchildren as the contingent beneficiaries. For deaths in late 2019, a child may be able to disclaim within nine months of the date of death and trigger stretch-out benefits under the old rules.

As always, tax and trust law is subject to change. Proposals of a reduction of the federal estate tax exemption to $3,500,000, higher progressive rates on estates, elimination of stepped-up basis upon death, and even the possible imposition of a California estate tax have all been considered by lawmakers.

We are dedicated to the planning and administration of estates for generations to come. We strive to understand and implement the goals of our clients as much as possible. It is our continued pleasure to spend time with our clients to adapt their wishes to the changing tax laws.

If you have an IRA or retirement plan we recommend more than anything else that you obtain from the IRA custodian or plan administrator a copy of the current beneficiary form. We urge all clients to send us copies of these forms.